Electricity in Russia’s Relations With Its Neighbours

Source of Integration, Influence and Income

One characteristic feature of the past year in Russia-EU relations is ever-complicating relations, which have direct impact on bilateral energy relations. A rather long-lasting story of European dependence on Russian gas; persistent discussions about the reliability of Russian gas supplies [note 1]; ongoing crisis in Ukraine and enhancing security of transit concerns [note 2], a range of sanctions a...

Source of Integration, Influence and Income

One characteristic feature of the past year in Russia-EU relations is ever-complicating relations, which have direct impact on bilateral energy relations. A rather long-lasting story of European dependence on Russian gas; persistent discussions about the reliability of Russian gas supplies [note 1]; ongoing crisis in Ukraine and enhancing security of transit concerns [note 2], a range of sanctions against Russia in relation to the Ukraine crisis [note 3] – a list long enough to think of self-dependence policy rather than integration projects.

Yet, in the situation of economic troubles, Russia is looking for opportunities to enhance its relations with direct neighbours, both in the West and in the East. This article looks at the prospects of such integration in terms of electricity trans-border flows. Is there space for development? Is the role of a ‘continental bridge’ feasible – for Russia and its counterparts?

Electricity in Russia’s energy structure

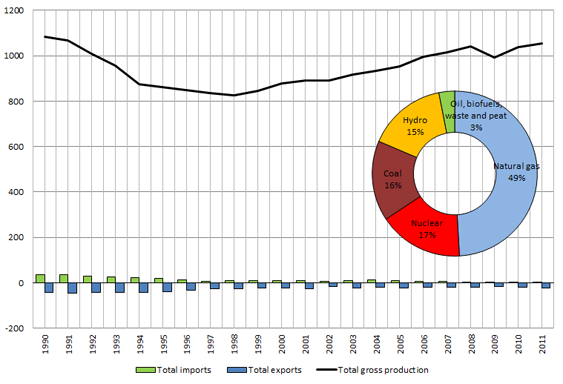

Let us start with the overview of the electricity sector. In 2012, power generation in Russia reached 1069,3 TWh (Figure 1). On the one hand, this is the highest level since 1991, but on the other, production level still has not reached the pace of the Soviet era. The infrastructure that exists since the Soviet period explains that output increase of 20,2% between 2002 and 2012 was feasible with only 3,8% addition in generation capacity [note 4]. On a global scale, Russia’s capacities are the fourth]largest in the world, in terms of the installed capacities, after the United States, the People’s Republic of China and Japan [note 5]. Economic reality permanently slows the outlook for electricity demand growth in Russia.

All these factors together make it logical for the country to be a net exporter of electricity – exports have actually decreased significantly as a result of the post-USSR reorganisation of the electricity networks (basically, a decomposition of the USSR unified electricity system). Exports in 2013 reached 17,5 TWh, which accounts for a small share of the overall electricity balance. Even though the total volumes are low, the cross-border supplies (targeted mainly at balancing) have been gaining prominence.

Throughout the first decade of the 21th century, Russia has undertaken a reform of the electricity sector [note 6]. As a result, large part of generation was privatised. One of the central developments was privatisation in 2007-2008 of the RAO UES (Unified Energy System), which was created in 1992 and was in charge of generation, transmission, operations control in the electricity sector, by 2007 it owned 72% of generation capacity and 96% of transmission lines, generated 70% of all electricity and about 30% of heat in Russia.

The regional vertically-integrated companies (controlled by RAO UES) throughout the 2000s were replaced by OGK (wholesale generating companies, each of them has power generation plants in different regions to minimise threats of monopolistic control), TGK (territorial generating companies, which unite generating assets not included into OGK and have a regional basis). There are still discussions of 'more than 70% of fixed assets being concentrated in the state-owned or state-controlled companies' [note 7], while foreign companies are not allowed to own more than 50% of TGKs, which are state]controlled, or acquire shareholdings in the transmission company [note 8].

The pricing was affected by the reform; the new market design for the electricity was meant as a transition to free]market pricing at the wholesale market by 2011 and at the retail market by 2015 [note 9]. It is often observed, however, that the current mix of pricing mechanisms provides unequal profitability within the electricity sector.

{kind=link}

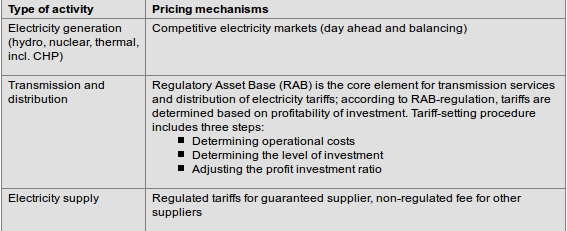

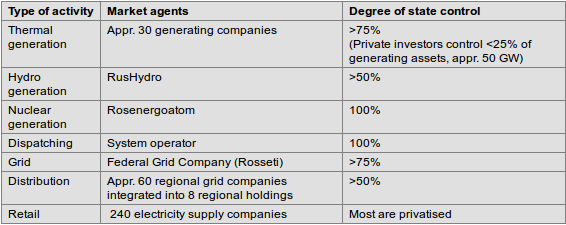

An evaluation of the electricity sector reform was provided by the director general of Rosseti (‘Russian Grids’) O.Budargin, who gave a speech at the European University at Saint Petersburg on March 3, 2015. He pointed out several problems. Firstly, there are currently different pricing mechanisms along the supply chain (in different segments of the supply chain, see Table 1). Secondly, requirements vary for actors active in the same segment of the supply chain (requirements varying for state entities and privatised entities, see Table 2). The third problem is closely connected to the first and deals with tariffs and the extent to which they are fair to customers, but also to different types of utilities [note 10].

Table 1. Pricing mechanisms in the electricity sector

Source: ERIRAS

{kind=link}

Table 2. State control in Russia's electricity sector

Source: ERIRAS

{kind=link}

Overall, this snapshot demonstrates that the result of the reform cannot be interpreted as singularly positive. As Budargin mentioned, 'the largest pitfall of the reform is that Russia has ‘exited the lift’ prematurely. Private generation works at the market rules. But the most crucial part – the transmission segment – is still facing a number of obstacles, not in the least obstacles of a regulatory nature. Transport is the priority not only for the electricity sector, it is an energy-sector-wide issue: destination and volumes of transportation are of ultimate importance, and transport infrastructure thus plays a central role. This can be proved by the following example. In 2009, an accident happened at Sayano-Shushenskaya hydropower plant, and instantly the electricity balance of the country lost 6000 MW, but no one even noticed it. It was possible to ensure uninterrupted supplies to end users because of (1) existing transmission grid interconnections inside Russia and (2) existing trans-border capacity with Kazakhstan' [note 11].

The core conclusions from this section thus are the following. There are preconditions for enhanced cross-border links in terms of spare generating capacity. Existing cross-border transmission connections proved to be of vital importance to Russia in terms of enhancing security of electricity supply. It is important that the supply chain - from generation to delivery to the customer - should work with the same rules and abide to the same authority. This is currently not the case in Russia. This may serve as obstacles to possible new trans-border engagements or further expansion of links that already exist.

Cross-border projects: Russia as the bridge

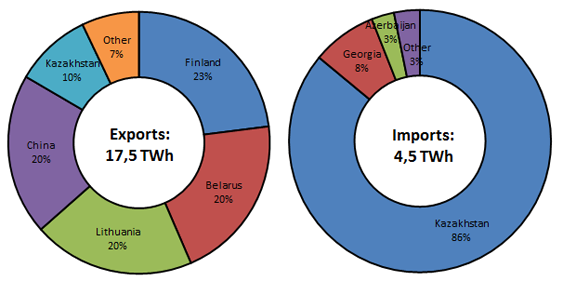

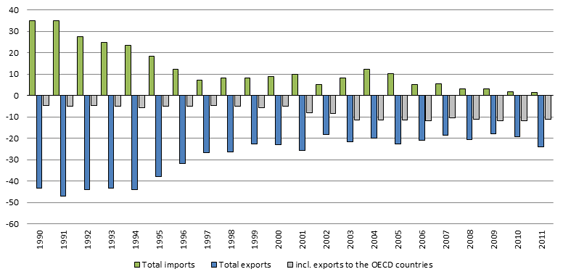

The Russian electricity supply network is connected to Baltic States (Estonia, Latvia and Lithuania), Belarus, Ukraine, Mongolia, Kazakhstan, Georgia and Azerbaijan [note 12]. Imports are carried from Kazakhstan, Geogia and Azerbaijan. The distribution of volumes is shown in graphs below (Figure 2). The volumes of exports and imports have declined after the collapse of the Soviet Union: the links that existed between ex-Soviet republics have diminished throughout the 1990ies with subsequent stabilisation in the 2000s; the structure has been changing with the increase of exports to OECD Europe (Figure 3).

{kind=link}

{kind=link}

The infographic below (Figure 4) demonstrates the essence of Russia’s potential as a ‘bridge’ between Europe and Asia. Firstly, the electricity grid connects the territory. Secondly, Russia itself is not a homogeneous market for electricity. The bulk of electricity is produced in the European part of the country, where the generation mix (as well as fuel mix overall) is dominated by natural gas. Siberia and the Far East, on the contrary, are dominated by coal use. This makes regions within Russia in fact similar to markets just across the border – on the Western side, Europe has a large share of gas fired generation; on the Eastern side, China has coal which dominates the fuel and electricity generation mix. Division between ‘Europe and Asia’ is clearly visible within Russia; the policy is targeted at enhancing the infrastructure links as well as developing the Eastern territories (this does not solely refer to the electricity sector – note such projects as East Siberia – Pacific Ocean oil pipeline, or Unified Gas Supply System). In relation to the geography of supplies, there are several issues to be noted.

{kind=link}

Sources: ERIRAS (figures and directions of export), IEA (map)

The Asian direction takes an important position in Russia’s electricity export strategy. China gains prominence and will most likely become the key partner in Asia in terms of electricity exports for Russia. 'Since April 2012, a new EHV 500 kV interstate overhead line (750 MW) has connected Russia (Amurskaya substation) with China (Heihe) through a back-to-back station (750 MW)' [note 13]. In 2013, Russian exports to China amounted to 3,5 TWh (compared to 1,2 TWh in 2011 as shown in Figure 4). There are also plans of constructing a subsea cable to Sakhalin and Hokkaido (Hokkaido-Sakhalin Cable System) [note 14]. Kazakhstan is one of the central partners currently, also ensuring further connections to Uzbekistan and Kyrgyzstan (which was caused by the split-up of the Soviet-time unified supply grid).

The European direction, as has already been mentioned, is leading for Russia’s cross-border grid connections and electricity flows in terms of volumes of supplies so far. This, it seems, falls within the initiative to develop the European electricity market. 'Why does Europe need energy interconnections? For electricity, the first is a matter of efficiency: more connections will allow more efficient plants to be used more widely by several states, adjusting at the same time national imbalances between offer and demand' [note 15]. If we stick with this logic – that more interconnections is better than less interconnections – it is surprising that Baltic states are implementing projects of compensatory networks in order to provide for electricity supplies without Russian ones. Russia is forced to build compensating networks as well in the North-West in order to compensate for a possible ‘divorce’ with the Baltic states. 'Neither they, nor Russia need this from an economic point of view', says Budargin on the issue [note 16].

It is logical for Russia to look for ways to become and enhance its role as ‘energy bridge’ in the Eurasian format, and its relations with Europe are really the key to it. Asian exports will go as far as the demand grows in that region; relations with Europe, on the contrary, are rather controversial.

A lot of infrastructure is already in place. Electricity, in case it receives the needed boost in terms of strategy within Russia, can become another source of integration, influence, and income.

The electricity sector in general (and not only in Russia) becomes more important as primary fuels are used decreasingly for final consumption and more for the transformation sector, including electricity generation. This is where the fuels are competing. Therefore, the electricity sector (domestic European generation and transmission) as well as electricity imports (as secondary fuel) gain relevance for regional gas and coal (and renewables) dynamics, particularly in the European market.

Electricity sector as the battlefield: interfuel competition

Russia's strategy should be to keep the existing interconnections, and enhance them. One suggestion is to study the issue of electricity exports instead of gas exports. Electricity cross-border flows have not created as much controversy as gas, particularly in relations with Ukraine [note 17].

From the energy balance perspective, it is the electric power sector, the largest of consumption sectors, that is the main field of competition between nearly all energy sources, and to a large extent it determines the dominant type of fuel at the present stage of energy sector development.

The electricity generation sector by itself is an area where fuels are competing with each other. Considering that there is a potential of energy saving and energy efficiency improvement in Russia, there may be possibilities of enhancing electricity exports. Moreover, 'recent economic development clearly demonstrates that profitability of gas generation in Europe is steadily declining, while profitability of coal-powered generation is growing' [note 18]. This is one reason for Russia to pay closer attention to coal exports, but also, electricity exports as final product.

Electricity as a secondary fuel/final product competes with primary fuels in such sectors as industry and commercial/residential. The electrification of all spheres of all human activity in general will have a range of far-reaching implications: in the long term available alternative energy resources and innovative new technologies can significantly increase both the economic viability of hydrocarbon reserves and the range of their interchangeability. But most importantly, they can also expand the bandwidth within which other energy sources (including renewables) can compete with hydrocarbons. This is why it is essential for Russia to be involved in the electricity sectors in the core regions of its presence – including Europe, including through cross-border transmission lines.

What role for Russia?

On the one hand, Russian supplies of primary resources for the European energy market – still a central part for the energy strategy and economic stability of Russia – seem problematic. 'What is wrong with Russian gas? It does not nicely fit into the European energy policy, which follows some clear (questionable?) political objectives. If all European security strategy in relation to gas markets and gas supplies will be centered on diminishing Russian supplies, Europe might find itself effectively solving this problem and yet remaining [even more] insecure' [note 19]. Clearly, there is a colossal amount of problems with gas exports.

Would it be possible to go for electricity export? 'Export potential is underutilised. The largest problem in this respect is competition between Rosseti and Gazprom. Rosseti is in favour of the unified electricity system on a Eurasian continental scale. Russia should play the role of bridge between Europe, Russia and China. But Europe is a difficult partner in building this bridge and finding solutions which would go beyond the current political leadership priorities' [note 20].

The most important advantage that Russia has is geography and the number of neighbours that it shares borders with. By simply developing the infrastructure, the country can capitalise. It is a promising perspective: Asia wants to trade with Europe, and Europe wants to have clean energy and pursue secure relations within the continent. Russia can serve as the bridge for both to reach their objectives. Quite clearly, the political climate in Europe is not favourable, but it is a political agenda, not an economic one.

Notes

1. Irina Mironova. What is wrong with Russian gas? European Energy Review. http://www.europeanenergyreview.com/index.php?id=4306

2. Miguel Martinez, Martin Paletar, Dr. Harald Hecking. The 2014 Ukrainian crisis: Europe’s increased security position. European Energy Review. March 19, 2015. /index.php?id=4348

3. Irina Mironova. Russia: Still-life under sanctions. European Energy Review. http://www.europeanenergyreview.com/index.php?id=4311

4. International Energy Agency. Russia 2014. Paris: OECD/IEA, 2014. P. 184.

5. Ibid.

6. Government Resolution No. 526 On the Restructuring of the Electric Power Industry of 11 July 2001.

7. Veselov F. Russian Electric Power Sector Overview. AEBRUS Seminar. Moscow, October 2013, http://www.eriras.ru/files/AEBRUS_25Oct13.pdf

8. Foreign Strategic Investments Law (2008, with amendments in 2008, 2011 and 2013).

9. Federal Electricity Law No. 35 of 26 March 2003, complemented by Federal Law No. 36 of 26 March 2003 On the Special Functioning of the Electricity Sector in the Transition Period.

10. Budargin Oleg. Russia’s Electricity Sector in the New Economic Reality: Act or Freeze? Public lecture at the European University at Saint Petersburg. March 3, 2015.

11. Budargin Oleg. Russia’s Electricity Sector in the New Economic Reality: Act or Freeze? Public lecture at the European University at Saint Petersburg. March 3, 2015.

12. International Energy Agency. Russia 2014. Paris: OECD/IEA, 2014. P. 187.

13. Ibid.

14. Ibid.

15. Lorenzo Colantoni. All you need is interconnection, or the key to success (or failure) of the European energy policy. European Energy Review. January 22, 2015. /index.php?id=4331

16. Budargin Oleg. Russia’s Electricity Sector in the New Economic Reality: Act or Freeze? Public lecture at the European University at Saint Petersburg. March 3, 2015.

17. Budargin Oleg. Russia’s Electricity Sector in the New Economic Reality: Act or Freeze? Public lecture at the European University at Saint Petersburg. March 3, 2015.

18. Mitrova T., Galkina A. Inter-fuel Competition. Higher School of Economics Economic Journal. 2013. Vol. 17. No. 3. Pp. 394-413.

19. Irina Mironova. What is wrong with Russian gas? European Energy Review. http://www.europeanenergyreview.com/index.php?id=4306

20. Budargin Oleg. Russia’s Electricity Sector in the New Economic Reality: Act or Freeze? Public lecture at the European University at Saint Petersburg. March 3, 2015.

Main image: D. Sharon Pruitt CC BY 2.0 license

{kind=link}