Long Term Outlook for Gas Demand and Supply 2007-2030

on

Long term outlook for gas demand and supply 2007-2030

Speech by Mr. Domenico Dispenza, President of Eurogas, delivered on May 5th in Brussels during a Eurogas workshop.

Ladies and gentlemen,

It is a great pleasure for me to be here today to introduce the result of a study made by this Association,

expected, I would say, with some interest by everyone in the gas business.

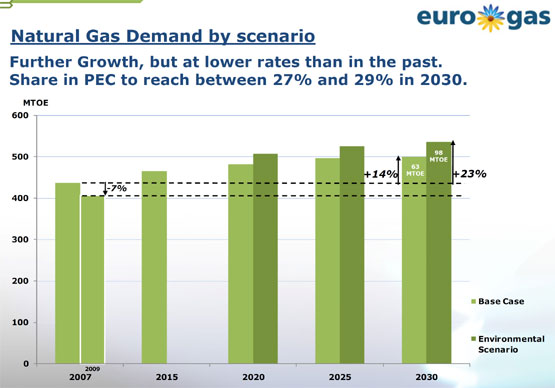

Today Eurogas will present a forecast, conducted on the basis of its own survey among its member companies, pooling their expertise, in order to provide the most realistic estimates over the long term. Two scenarios will be presented: a base case vision and an environmental alternative, which will say how natural gas can contribute more to a sustainable energy supply in the 27 countries EU. This, I would like to repeat, is the shared European gas industry vision.

After years of almost uninterrupted growth, the European gas industry for the first time faced severe sales losses last year. The EU gas demand for the first time experienced a material and not weather related, drop of 6,4% resulting mainly from the economic crisis. This analysis has been published by Eurogas, available to everyone. A slight upturn in demand is expected in 2010 – we have seen this in the first months - and must be monitored with attention in its unfolding. Despite these early signs of recovery, our expectations regarding long term demand have been substantially revised downward in the last year, with obvious consequences over supply/demand balance.

Nevertheless, because of its "green properties", highly efficient application technologies and flexibility, natural gas consumption in EU member states is still expected to rise between 14% and 23% in year 2030 in comparison with 2007, that is, to a range between 500 and 535 Mtoe from 2007’s 437 Mtoe depending on the two scenarios. If we want to speak in the more common unit for the gas world, that is billion cubic meters we would arrive to, respectively, 595 and 637 bcm from the 2007’s 520.

|

In our results we clearly see a phenomenon which is more and more evident, that is a certain erosion of the link between energy consumption and economic growth. This is a consequence of the investments in energy efficiency. Such investments, already spontaneous feature of an increasingly mature European consumer base, have gained further momentum from the effort to respect climate change commitments mandated by the EU.

Let’s look briefly to gas market segmentation:

In the residential and commercial sector, gas is now the market leader with a market share of approx. 35%. Given a faster market penetration by highly efficient heating technologies, the contribution made by gas to supplying the space heating will be stable in the long run at a level of 170 mtoe.

Gas currently accounts for 31 % of industrial final energy consumption. Depending on economic developments and the price competitiveness of gas, sales to industry could increase by 5-10% in 2030. Today, gas-fired power stations produce one fifth of the electricity in the EU27. Gas offers considerable potential for further reducing CO2 emissions in power generation in a most flexible manner and in very competitive conditions. Natural gas can deliver full stability, abundance and security to both future European energy mix and to our overall economy.

Gas, in combination with biogas, has other key potential developments, for example as a highly competitive transport fuel and in low energy building projects.

As to the supply side, the European gas market has gone, during the past months, through a phase of deep change induced by the global economic crisis we still live in.

Of particular relevance are the developments underway in the North American market. A local recession and related flat demand, combined with a sharp increase of domestic unconventional gas production, is having a major impact both regionally and on the world LNG trade. Events like the almost total stoppage of Canadian gas exports and the proposed conversion of some US LNG import terminals into export facilities show the depth and speed of changes which impact on the global natural gas industry.

Such global turmoil in market dynamics has triggered a series of consequences inside the European market and in the relationship with our external gas suppliers.

Substantial volumes of spot gas are made available in some European hubs meeting the demand, while the bulk of long term oil-indexed European supply contracts still maintain the traditional relatively small flexibility. This determines unprecedented peaks of liquidity and churn.

Therefore, pricing paradigms in most of national markets are being somehow challenged by such wave of relatively cheap gas, determining calls for formal de-linking from oil. At the same time, the main gas exporters are seriously discussing among themselves and with their long term buyers how to manage the current oversupply.

Notwithstanding such turmoil, we must remember that natural gas reserves are abundant worldwide and are estimated to be able to meet global needs for at least another 60 years. Moreover, conventional natural gas resources could, at a certain point in the future, be to some extent complemented by unconventional resources within Europe, should the appropriate conditions be met.

Of course it is hard and almost useless to predict the future, but some short and medium developments can be reasonably inferred:

- gas will continue its path towards commoditization and more global circulation, mainly thanks to the surge in LNG availability and to the necessity for both long term sellers and buyers to optimize gas value in a rapidly changing market environment,

- current discussions on long term contracts may be seen affecting the buyer/seller relationship, a

relationship that will anyhow remain a pillar of supply security, - in a wider perspective, gas will have to continue competing with the other primary energy sources in a more uncertain context, providing at the same time structural synergies with renewable sources.

I believe that the pivotal role of gas in a lower carbon European economy will be maintained and even

reinforced. The virtues of natural gas as by far the cleanest and most flexible fossil fuel available are unquestionable. Such virtues, coupled with the skills of a robust industry and with an enhanced dialogue with producers, will further contribute to reaffirming its importance.

Clearly the gas business is governed by both long term and cyclical factors. The current situation of oversupply will be over in a few years. As the gas business is a long-term one, investments are necessary today. The European gas companies need therefore a stable and predictable regulatory framework allowing them to undertake the important investments required to ensure the future supply/demand balance.

To conclude, at the end the “market” will decide on the merits of each primary energy source. In this respect we hope that today’s presentation of the outlook 2030 will create a better understanding of the unique perspectives offered by natural gas in the context of a balanced, sustainable and more secure energy mix for Europe.

Thank you.

You can find the full report here.

Discussion (0 comments)