FCNG: A Solution to Unlock the Full Potential of East Med Hydrocarbons

The recent discoveries of large hydrocarbon reserves in the Levant basin in Eastern Mediterranean, have transformed the region to a potential net exporter of natural gas. The successive discoveries of Tamar in 2009 and of Leviathan in 2010 in Israel’s EEZ totaling almost 28tcf of natural gas, followed in 2012 by the discovery of Aphrodite in Cyprus’ EEZ with 4.5tcf, created euphoria as to the region’s potential to become a serious player...

The recent discoveries of large hydrocarbon reserves in the Levant basin in Eastern Mediterranean, have transformed the region to a potential net exporter of natural gas. The successive discoveries of Tamar in 2009 and of Leviathan in 2010 in Israel’s EEZ totaling almost 28tcf of natural gas, followed in 2012 by the discovery of Aphrodite in Cyprus’ EEZ with 4.5tcf, created euphoria as to the region’s potential to become a serious player in exports of LNG to global markets.

Cyprus’ ambition was to turn the island into a regional energy hub by constructing a land based LNG Export Plant at Vasilikos, in the south of the island. A feasibility study carried out in 2012/13 by Noble, the major upstream operator in all three gas finds, estimated the cost of a two train liquefaction plant to be about US $9 billion. The plan was to supplement feedstock gas from Aphrodite with gas from Leviathan. Whilst Israel was interested to supply the additional gas in 2012 and 2013, the opportunity was missed and Cyprus’, as well as the region’s, aspirations for an LNG export plant were cut short.

But hopes to construct a land based LNG Export Plant suffered yet another telling blow as oil and gas prices plunged to new lows, casting shadows over the profitability of new LNG projects. The crisis in oil and gas prices also shelved, at least for the time being, any thoughts for a Floating LNG plant, as LNG exports to Asia or Europe could not sustain the considerable capex involved.

In the meantime, Noble/Delek revised their monetization plans of the natural gas reserves in Aphrodite and Leviathan, turning to exports via pipelines to Regional Markets, and more specifically Egypt. To this effect, numerous MoUs have been signed between the governments of Cyprus and Egypt as well as between the Leviathan partners and Egyptian companies.

The crucial question remains, however, as to whether, under the circumstances, supplying Egypt is commercially viable for the stakeholders involved and the best option for Cyprus’ current proven reserves of 4.5tcf of natural gas.

In our analysis, here below, we demonstrate that gas exports to the Egyptian market and/or to Egypt’s LNG export plants cannot be a viable export option for reasons which we explain. Moreover, we demonstrate that, under the circumstances, the best option for Cyprus is to export its natural gas to Europe by Floating Compressed Natural Gas (FCNG) via Greece.

Exports by pipeline to Egypt

At first, we must clarify that the need to import gas for domestic use in Egypt is short term, as Egypt has proven untapped hydrocarbon reserves of the order of 77tcf. Underscoring this fact is the Egyptian government’s recent declaration that its target is to become self-sufficient in natural gas within the next 4-5 years, thus, meeting the current shortfall in supply from its own reserves and thereby ending the import of LNG. Towards this target, the Egyptian Government has adopted a proactive policy towards IOCs comprising the repayment of old overdue debts and the increase of the price paid to producers from $2.65/MMBtu to $3.95-$4.88/ΜΜBtu, intended to encourage the latter to increase their E&P investments and ultimately their current production.

Evidently, the need to import gas for domestic use in Egypt is short term and this in itself makes an underwater pipeline commercially un-bankable since project financing would necessitate a period of supply of 15-20 years for the monetization of 90% of the reserves, i.e.7-8bcma.

In addition, domestically produced gas would cost from $3.50 to $5.00 per MMBTU, whilst gas piped from Cyprus at $7-$8.would be expensive in comparison to Egyptian gas, and by the time the Aphrodite project is completed (the earliest in 2019), Egypt will no longer require gas imports.

Subsequently, any natural gas export to Egypt would be directed to one of the two LNG Export Plants, namely BG’s Idku, which is underutilized due to lack of feedstock gas. Already, however, BG has signed a MoU with Noble/Delek for 5MT per year and is negotiating with BP the supply of an additional 2.5MT per year feedstock gas from Leviathan and West Delta Deep Marine (WWDM) respectively, which essentially means that Idku, with an ability to produce 7.2MT per year, will be filled to capacity. As the legal dispute between Noble/Delek and Israel’s Anti Trust Authority is soon coming to an end, gas will start flowing by pipeline from Leviathan to Idku and this alone will exclude natural gas from Aphrodite, since the latter’s development would necessitate a minimum export quantity of 7bcma in order to be commercially viable.

Moreover, since BG’s takeover by Shell, the latter may decide not to proceed to have commercial dealings with the Republic of Cyprus (RoC), fearing that such dealings will jeopardise its interests in Turkey, a country whose policy has been overtly hostile to Cyprus since WWII. Turkey is a rising market for natural gas and Shell wants to continue to be a key player in the Turkish market.

Obviously, there are still preconditions and impediments which need to be overcome in order for Cyprus gas to flow to Egypt by pipeline. With the current state of play in the East Med the likelihood is that this will not happen.

In such an event, Cyprus will have no other option but to turn for exports to other regional markets, namely, to SE Europe using the technology of marine CNG, via Greece.

Greece: a regional gas hub

Greece today has one LNG import terminal in Revithoussa and plans to construct two more in Northern Greece, namely, the FSRUs in Kavala and in Alexandroupolis. These projects, underpinned by strategic gas infrastructure such as interconnectors and pipelines as per Table 1, will contribute to the energy security for South East Europe, and differentiate energy sources, in line with the EU’s priorities to strengthen energy security and union.

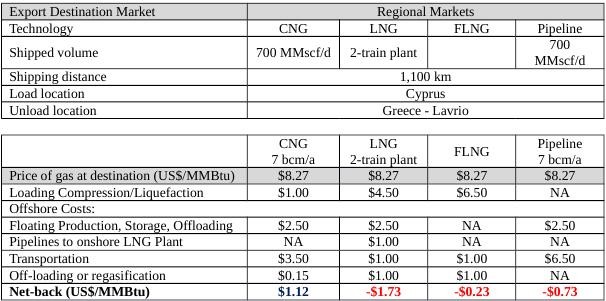

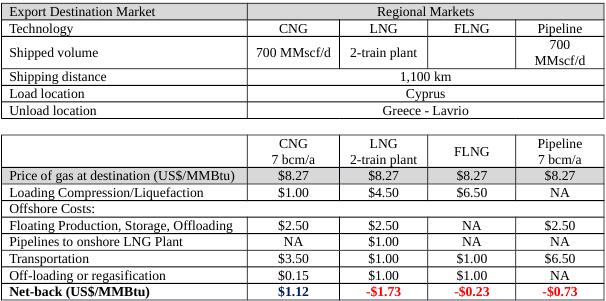

Greece, however, is at the same time an ideal destination for FCNG from East Med gas finds, as it lies at a distance of 2200km, within which FCNG is cost effective as underlined in Table 2 by the Netbacks to operators from different technologies.

The combination of LNG and CNG receiving terminals will clearly give Greece a comparative advantage. Gas from Aphrodite could be supplied to these countries by FCNG as early as 2020. Given current proven reserves this could be 7-8 bcma, with the potential to grow, sufficient to make an impact in SE European markets such as Bulgaria, Romania, Serbia and Hungary.

Table 1. Strategic Infrastructures which will add value to East Med Hydrocarbons transported to Greece

Table 2. Net-backs to operators from shipping natural gas to Greece applying different technologies. Source: Sea NG Alliance, Information on Eni's FLNG in Mozambique, Public Information

Notes to Table 2:

1. European Union Natural Gas Import Price in March 2015 was at a current level of 8.27 down from 10.88 one year ago. This is a change of -23.99% from one year ago.

2. Contract term of 20 years following three years build period

3. Loading and unloading equipment located on-board CNG ships. SAL buoy loading & offloading for CNG (> 300 meter water depth)

4. Block 12 proven reserves to be 4.8tcf x 28.31bcm/tcf = 135.84bcm/20 years as per contract term i.e approx. 7bcma

5. 13% unlevered IRR

6. Pipeline Capex of $6.5 million/km for deep water. No Opex included

7. Gas consumed as fuel valued as shrinkage

8. Gas composition typical of Eastern Med

9. FLNG based on Mozambique FLNG by Eni - Capex $1billion/mpta

10. Pipeline Capex of $6 million/km for deep water. Opex included and assumed at 2% of capex/a

FCNG: A politically appropriate technology

During recent years many experts have advocated for a pipeline that would transport Cyprus and Israel natural gas via a pipeline through Turkey and from thereon to Europe. The prospects of this is option are, however, very gloomy given the state of play in East Mediterranean politics between Israel, Greece and Cyprus with Turkey.

With marine CNG, on the other hand, sea borne transport of natural gas from Leviathan and/or Aphrodite to Turkey will be possible as there will be no bilateral issues arising from EEZs involved, nor will the export countries feel permanently tied down to a fixed destination with geopolitical implications. Moreover, FCNG requires no upfront capex by the companies, as do pipelines. Thus, marine CNG would be an optimum solution for all the stakeholders and the countries. More specifically,

For Israel and Cyprus FCNG technology means:

Unlocking the development of the Aphrodite and/or Leviathan reservoirs

Unlocking new markets such as Greece, Jordan, Italy, Croatia, even Turkey

Flexibility to supply alternative markets compared to a fixed pipeline from East Med to Egypt or Turkey.

For Turkey FCNG technology means:

Additional sources of natural gas

Increasing the energy security for the country

Therefore, FCNG can be a politically appropriate option for both Cyprus as well as Israel given East Med’s entrenched politics.

CONCLUSION

The commercial development of East Med natural gas cannot disregard the region's entrenched politics nor can it ignore the interests of the upstream companies and this makes the stakeholders’ task both complex and challenging as they are confronted not only with geological and commercial issues and risks that need to be addressed, but also with the political perplexity which impede potential synergies. The region needs optionality and cannot afford to put all its gas export “eggs” in one basket.

The roadmap to the monetisation of East Med Hydrocarbons clearly indicates that the region, together with the upstream contractors, must develop its hydrocarbons’ potential in a flexible and time sensitive manner, while maximising the economic benefits. Pipelines do not provide that flexibility.

East Med gas requires careful planning of long-term strategy and thus dictates a more creative approach. FCNG will be a commercially viable method which, whilst taking into account the region’s political volatility, will not impose limitations on destination markets, but instead offer the flexibility of regional exports, thus offering a better market positioning for East Med Natural Gas. In turn, this will allow all stakeholders to maximize their returns.

Clearly, East Med geography, geology and politics require the offshore flexibility of regional FCNG. This technology is by far the optimum and politically appropriate solution. all stakeholders

Athanasios Pitatzis is Member of the Greek Energy Forum. The opinions expressed in the article are personal and do not reflect the views of the entire forum or the company that employs the author. Follow Greek Energy Forum on Twitter at @GrEnergyForum and Athanasios at @thanospitatzis.

Christis Enotiades is the Chief Operations Officer of East Med Investment Advisory Services Ltd – eMIAS- The opinions expressed in the article are personal and do not reflect the views of the entire forum or the company that employs the author. Follow Christis on Twitter at @chrienot.

This article is part of the knowledge partnership between European Energy Review and the Greek Energy Forum a group of energy professionals sharing common interest in the broader energy industry in Greece and South-eastern Europe.

Elektor Magazine has been one of the leading sources of information on electronics for engineers, designers, start-ups and companies for 65 years. Our magazine is powered by an active community of electronics engineers – from students to professionals – who are passionate about designing and sharing innovative ideas.

For them, we publish hundreds of items a year, in formats such as articles, videos, webinars, and other learning formats. Our mission is to share knowledge in every possible way and inspire readers with the latest developments within the electrical engineering sector.

Thank you for your vote!

Leave further comments in the fields below.

Thank you for your vote!

If you wish to leave a comment with your rating, please first use the login below. If not, just close this window.

Discussion (0 comments)