A novel approach to the RES promotion

on

A Novel Approach to RES Promotion

In March 2015, the Polish Parliament passed a new law relating to renewable energy sources (RES). The law aims to promote mini and micro-installations introducing incentives for individual customers who decide to produce electricity for their own use and sell the excess energy to electricity markets. These customers are called 'prosumers' as they combine electricity consumption with production. The novel approach to prosumers introduced in the new RES law is worth analysing, particularly regulations concerning micro-installations; those up to 3kW and mini-installation of 3-10kW rated capacity.

Previously, any activity relating to energy production, transmission and trade in Poland has been licensed by the energy regulator and required registration as a commercial entity with the tax authority, specifically for the payment of Value Added Tax (VAT). All companies must fulfil these regulations, regardless of size, from sole traders to large, publicly traded corporations.

The new RES law exempts prosumers from licensing and VAT registration. They are also not required to obtain permission from their distribution company to connect mini and micro-installations to the electricity grid. The only requirement imposed on prosumers is to inform their local distribution company that the installation is commissioned and produces electricity.

The incentives for prosumers include generous feed-in-tariffs granted for 15 years, net metering and investment subsidies from the National Environmental Agency, which cover up to 40% of the cost of investment.

|

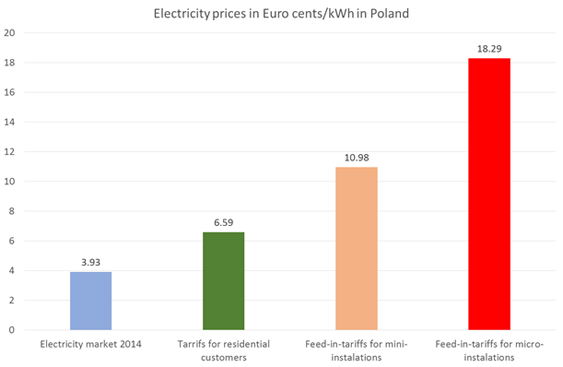

Typical electricity prices in the wholesale electricity market oscillate around €0.04 per kWh. Electricity prices for residential customers vary between €0.06 and €0.07 per kWh. The new RES law established a feed-in-tariff for mini-installation (3-10kW) equal to about €0.11 per kWh,

| the sale of electricity by prosumers is settled according to ‘net metering’ |

For example, a prosumer with a micro-installation of 3kW of photovoltaics will produce and sell electricity during the daylight hours of relatively low consumption – especially for residential customers, but with net metering, this production will be subtracted from his entire consumption, including that during peak hours and high prices.

Prosumers also pay smaller transmission fees as most delivery tariffs depend on the amount of electricity taken from the power grid. All above incentives, including support for investment will reduce the pay-back period for prosumer installations to less than 5 years.

Provisions in the RES law set the total amount of micro-installations which are able to get the generous feed-in-tariffs to 300MW of rated power for the entire country. Similar constraints are imposed on mini-installations for which the total rated power cannot exceed 500MW.

| incentives, including support for investment will reduce the pay-back period for prosumer installations to less than 5 years |

The position of the Tax Office is still unknown as to whether the production of electricity by individual energy prosumers will be subject to income tax, as it is not possible to charge a VAT to unregistered producers. Perhaps the Tax Office will forego taxing prosumers’ electricity production altogether, although this perhaps is wishful thinking.

| Wladyslaw Mielczarski is a Full Professor in Power Engineering at Institute of Electric Power Engineering, Lodz University of Technology, Poland, www.mielczarski.neostrada.pl |

Discussion (0 comments)