European climate policy must distinguish between East and West

on

European climate policy must distinguish between East and West

EU energy and climate policies are exerting a disproportionate burden on the economies of Central and Eastern European countries. This is leading to growing discontent and opposition in these countries. The only way that unity can be maintained, argues Friedbert Pflüger, is a new approach within the EU on energy and climate policy that takes the needs and interests of Central and Eastern European states into consideration.

|

| (c) BNR |

Having been a discussant at two energy conferences in Prague and Katowice recently and following closely the debates in Central and Eastern Europe, I have come to the conclusion that we are witnessing growing discontent within the new EU member states concerning the energy and environmental policy of the European Union.

This is not only true for the specific instruments and measures coming from Brussels; it also applies to the values and aims proclaimed by the European Commission and the Council of Europe. The Polish government’s veto in June 2011 regarding the European Commission's Low Carbon Roadmap for 2050 and its firm stance against any higher EU reduction goals until 2020 are no accidents. These decisions probably mark the beginning of intense debates, if not confrontation, within the European Union. In order to maintain unity and enable policymakers in Brussels to pursue a common energy strategy, it is necessary to listen carefully to these signals and attempt as quickly as possible to understand the specific challenges facing Central and Eastern European countries in order to meet the proclaimed aims of the Union.

The EU Energy Roadmap 2050, adopted on December 15, 2011 by the EU Commission and strongly supported by Germany and France, is undoubtedly an impressive document. It is a resolute attempt to find a common ground for an EU energy policy which merits the name. Its main author, EU Energy Commissioner Günther Oettinger, deserves much credit for this important impulse. He has a high reputation in Central and Eastern Europe, because his statements tend to reflect an understanding of economic and structural connections as well as a sense of the needs of the business community. There are high hopes that he will be able to serve as a bridge between those in the EU who mainly think of climate change when they talk about energy and others who associate energy more with supply security and competitiveness. The expectation of the Central and East European countries is to bring these aims into more balance.

The proposed EU Roadmap sets emission reduction targets up to 2050, aiming at an EU-wide target of 80-95% below 1990 levels by 2050 and a specific target of a 93-99% reduction in greenhouse gas emissions in the power sector. By adopting additional regulations on environmental objectives, the Commission has put significant obligations on member states.

But these obligations are increasingly being perceived by Central and East European states as unfair. While the EU’s climate and sustainability concerns are legitimate and require effective policies, it is just

| These obligations are increasingly being perceived by Central and East European states as unfair |

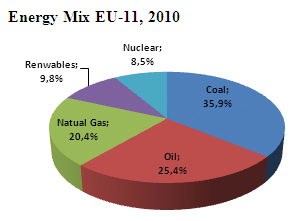

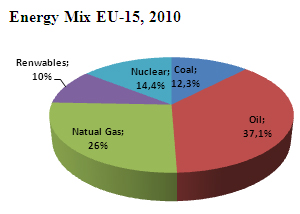

The EU-11 – Bulgaria, Croatia, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Romania, Slovakia, Slovenia – are what the Ernst & Young report has dubbed the new member countries to explicitly differentiate them from the EU-15. According to the report, the energy mix of the EU-11 differs considerably from the EU-15. The EU-11 has:

- A significantly higher share of coal than in the EU-15 (almost 36% compared to only 12.3%, for the EU-15)

- A lower share of nuclear power (8.5% versus 14.4%)

- A considerably lower share of petroleum products (25.4% vs. over 37%)

Both the higher share of coal and the lower share of nuclear power in the EU-11’s gross inland consumption of energy are major grounds for the higher carbon intensity (emissions of CO2 in relation to energy consumption) of their economies.

|

|

| Source: Own chart; Data from Ernst & Young Executive Summary to the Report: 'Introductory analysis of EU-11 countries energy sectors', 2012 |

The higher share of coal makes most of the new member states more vulnerable to stricter EU environmental protection policies. In Poland, for example, the general consensus is that EU climate policy will lead to considerably higher electricity prices and thus the migration of important industries. A report by the World Bank (Transition to a low-emissions economy in Poland) concluded that the EU’s climate policy will cost Poland 1.5 to 2.2 percent of its GDP until 2015 and 1.8 to 3.1 percent for 2020. Abatement measures are also expected to have a negative effect on employment, with an employment loss ranging from 0.2% up to 7.4% between 2015 and 2030. Moreover, the Polish Chamber of Commerce has estimated that implementing the Roadmap would triple or even quadruple energy prices after 2020.

In an interview with the BBC, Polish environment minister Marcin Korolec stated: "For countries like Poland such a reduction (in emissions), with our starting point today of basing 93-95% of our electricity from coal, would mean, firstly, extremely high prices for electricity in 2050, and secondly, the transfer of industry outside Poland's borders. This is not acceptable because we are and want to remain an industrial country. Our main strength today is that we are part of industrial Europe and this is part of Poland's success.”

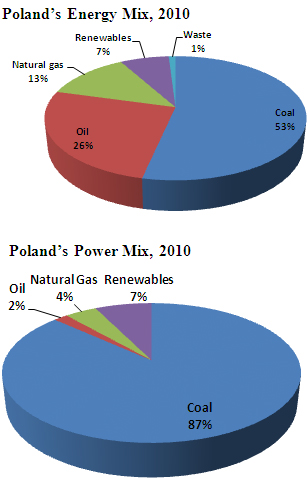

The motives that prompted Warsaw to veto the EU’s climate aims become clearer (and perhaps more

|

| Source: EU Commission (http://ec.europa.eu/energy/observatory/countries/doc/2010-country-factsheets.pdf) |

understandable) when looking at Poland’s specific energy mix.

This clearly illustrates the difficulty for the Poles - and the situation is not very different in most of the other new member states. The starting position concerning reduction targets differs considerably from that of the older members - because of Poland’s dramatically different energy mix. In addition, given the fact that the EU-11 still have a long way to go until they reach the average EU GDP per capita, one can understand the enormous challenge in attempting to meet the EU's climate goals while trying to catch up with Western European countries economically.

The economic standing of the EU-11 is still far behind the EU average – an average GDP per capita of €9,000 in 2010 represented only 32% of the EU-15 average (the EU-11 average GDP in purchasing-power parity in 2010 amounted to €14,7000, which represented 54.9% of the EU-15), according to the Ernst & Young report.

Hot issue

Before all this becomes a real hot issue for the headlines of newspapers and a burning subject at EU summits, one should carefully try to build bridges, find compromises and help the new members to find ways to meet the ambitious EU targets. It is therefore necessary to formulate a new strategic consensus within the EU on energy and climate policy.

Firstly, the issue of climate change should be kept on the agenda. It remains serious despite a paradigm shift that has virtually put the matter on the backburner in view of the current economic problems gripping the EU. It is important now not to let the pendulum swing in the other direction. A healthy balance between the EU’s three primary energy policy objectives of sustainability, security of supply, and competitiveness must be maintained.

Secondly, efforts should be made to make coal a cleaner energy source. According to a joint study by

| Before all this becomes a real hot issue for the headlines of newspapers, one should carefully try to build bridges, find compromises and help the new members to find ways to meet the ambitious EU targets |

Hence, it is all the more important that the continued use of coal take place in a responsible and sustainable manner that seeks to minimize its carbon footprint. This involves using coal in combination with efficiency enhancing technologies as well as technologies such as carbon capture and storage (CCS).

In Poland, for instance, more than 50% of the power stations are over 25 years old and have an average efficiency rate of 36%. This presents a great opportunity for Poland's older power plants to be replaced by newer and significantly more efficient power stations. The current state-of-the-art power plant technology has an efficiency rate of around 45%. This could allow a reduction of 20% in CO2 emissions if old power plants were replaced by modern lower emissions technology. To incentivize the construction of coal power plants with an efficiency of approximately 45% or more, one policy option would be for the EU to provide tax incentives for new power plants based on coal with the efficiency of a minimum 45% to those countries willing to make the necessary investments.

Developing CO2 mitigating technologies like CCS is just as essential, not only to meet sustainability targets here in the EU but also to limit emissions worldwide through the export of such technologies. This is why it is important that projects like the Belchatow CCS plant continue to receive EU support. Operator PGE has said it will not move forward with this project without additional assurances from the Polish government and other EU states.

Thirdly, alternative indigenous sources of energy like shale gas, tight gas, shale oil and tight oil also stand to play an increasing role in contributing to sustainability and energy security objectives as their exploitation potential continues to be explored. With about half the CO2 emissions of coal, increased natural gas use can drastically reduce carbon emissions. In the US, greater natural gas use as a result of the shale gas revolution has already lowered CO2 emissions by almost 8% in just five years.

The development of the vast shale gas reserves in Central and Eastern Europe, especially in Poland, has enormous potential. The U.S. Energy Information Administration (EIA) estimates that Poland has

| In Poland more than 50% of the power stations are over 25 years old and have an average efficiency rate of 36% |

Fourthly and lastly, the large regions of available and arable land and a generally favorable regulatory environment in some EU-11 states provide very good conditions for the further expansion of biofuels as well as wind and solar energy.

Biofuels can help reduce the dependence on fossil fuels while substantially cutting CO2 emissions in the transport sector. Companies today can produce biofuels with up to 90% less CO2 compared to regular gasoline and diesel. This exceeds the statutory demand to cut CO2 emissions by at least 35% compared to fossil fuels. Especially second generation biomethane produced from organic wastes such as sewage, manure, food wastes, and landfills can help curb CO2 emissions while avoiding the food vs. fuel debate.

The prospects for wind power generation in the EU-11 are also excellent due to a favourable regulatory framework in some countries and considerable wind energy resources. Offshore wind development in Poland, for instance, could greatly contribute to the country’s efforts to meet sustainability targets while creating new employment opportunities.

The potential for solar power generation should also not be underestimated, particularly in countries like Bulgaria. Poland (which is currently Europe’s largest electricity market without photovoltaic development) and Romania also have untapped potential.

In light of the significant differences between the EU-11 and EU-15 in terms of the level of economic development and the structure of their energy sectors, it is essential that EU energy policy balance the objectives of energy security and sustainable development while avoiding adverse effects on the competitiveness of European economies. A balanced policy requires different approaches for the EU-15 and EU-11 - one that does not exert a disproportionate burden on the economies of the Central and East European countries, or any other state for that matter. This would entail adopting a more integrated and flexible approach that takes the specific needs and requirements of each member state into consideration when implementing policies.

|

About the author Friedbert Pflüger is Professor and Director of the European Centre for Energy and Resource Security (EUCERS) at King’s College London and CEO of Pflüger International Consulting. He is also a senior advisor to Central Europe Energy Partners (CEEP), a non-profit association that represents the interest of the energy industry in Central and Eastern Europe. |

Discussion (0 comments)