Defending Market Share: A Dilemma for OPEC or for Shale Oil?

June 17, 2015

on

on

The sustained higher oil prices provided an excellent breeding place for a technology that has been around for many decades – hydraulic fracturing to nurture and prosper. As a result, US shale oil production increased from 1.24 million barrels daily (MMBD) in 2007 to over 4.72 MMBD at the end of 2014.

The sustained higher oil prices provided wind falls to major oil producers but at the same time severely affected the global economies, particularly oil importing countries. For oil producing countries more revenues means more resources for the development of their economies and therefore generally ignore its implications for global supply and demand. The sustained higher oil prices not only negatively effected the demand side, it also created a glut in oil market – eventually leading to collapsing oil prices.

Most of the OPEC members require continuous massive cash flows because they are in the process of economic development. When oil prices are high there are no issues, however when oil prices are suddenly in free fall this poses a real challenge. Challenges for OPEC members in 2015 are even more difficult then they were in the past as they are fighting three conflicting fronts: meeting ever increasing cash flow requirements; defending their market share in a a low oil price environment; and dealing with the competition of the US booming shale oil industry. In the past, OPEC has been pursuing a policy of stabilizing the market by increasing/decreasing production quota but at the same time defending its market share.

For example, strategy in 2015 is different from the one in the 1980s when OPEC increased its production to regain its lost market share due to significant increase in Norway and UK oil production, resulting in collapsing oil prices in 1986. Whilst in 2008, OPEC twice cut its production in an effort to arrest the free fall of oil prices. During recent meetings OPEC has been maintaining a production quota of 30 MMBD as oil prices remained above $100/BBL and even when oil prices plunged below $60/BBL. For example, during the 166th meeting held on Nov 27, 2014 and the 167th on June 5, 2015, OPEC members unanimously agreed that the global oil market is well supplied, inventories are higher than the previous five years average and therefore they would stick with 30 MMBD production quotas.

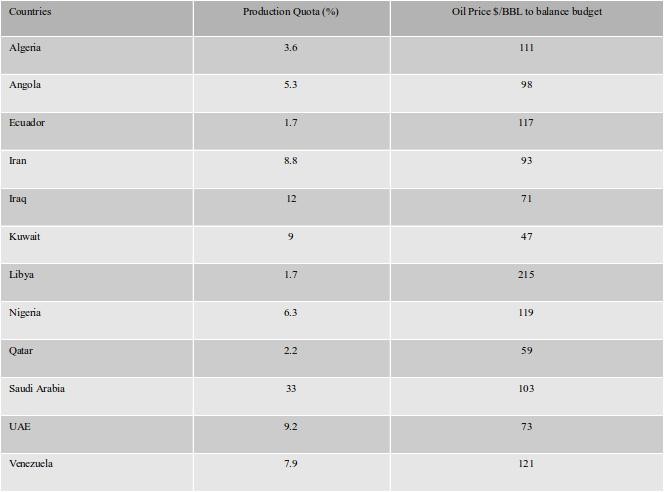

The next meeting will be held on Dec 4, 2015. With this announcement the element of uncertainty is reduced and one can see the determination and commitment of OPEC members to defend their market share even at the cost of lower oil prices. OPEC probably isn't interested in further increasing its production like in the 1980s or cutting its production for a revival of oil prices (2008). The problem is that OPEC is now facing a Catch-22 situation. On the one hand OPEC members need more revenues to meet their ever increasing government budgetary requirements but lower oil prices prevent that from happening. On the other hand if OPEC cuts its production in an effort to revive oil prices it is threatened by losing market share to US shale oil. At oil prices of, for example, $65/BBL (Brent May 2015) OPEC members would be needing substantial higher oil prices to balance their budget (see Table 1). Only Kuwait and Qatar would be in a position to meet their cash flow requirements, the other members would have to produce more or withdraw from sovereign funds in order to balance budget.

Table-1: OPEC production based on quota and oil prices to balance budget*

*The respective shares of the group’s supply are based on April levels. The estimates for the price per barrel each member needs to balance its budget are from the International Monetary Fund unless stated otherwise.

Source: Gulf Times: Saudi oil strategy seen prevailing in Vienna: OPEC reality check

So far so good. OPEC is successfully maintaining its production quota of 30 MMBD (though there is news they are producing more) that allows it to maintain its market share, and also deter the rising US shale oil production threat. The real challenge however, for OPEC, is how to deal with Russian increasing oil supplies. Russia hit hard by sanctions, requires more revenues to aid its crippling economy – by increasing its oil production. According to Bloomberg in May 2015, it extracted 10.7 MMBD, compared with Saudi Arabia’s 10.2 MMBD. It was the first time Russia took the global lead since 2010.

In addition to Russian oil supplies, another challenge for OPEC is how to deal within its own group. That is, what will happen when economic sanctions on Iran are lifted? A number of countries/companies are already lining up in Iran to seize this investment opportunity. Experts estimate it will take a year or so before Iranian oil production of over one MMBD will hit the market (there are divergent views about quantity and timing). And what would happen if the situation in Libya and Iraq would also simultaneously improve? What would be the implications for global oil supplies and the other OPEC members? Iran and other war torn countries would require huge cash flows for the redevelopment of their economies. How will they finance that? By selling more oil than the allocated quota in a regime of lower oil prices.

More oil supplies from OPEC and Russia are likely to further depress oil prices and this probably temporarily reduces some of the US high cost shale oil production. As a consequence OPEC members face the difficult question how to provide the desired cash flows to their respective governments. In the absence of resilient global oil demand OPEC members will have to dip into their sovereign funds. If OPEC members adhere to production quotas and keep oil prices below the magic number of $60/BBL it will probably discourage US shale oil production at least in some of the basins as well as discourage shale oil development in rich resource countries like China (Table 2). Just like technological advancement in horizontal drilling and hydraulic fracturing turned out to be a nightmare for OPEC, OPEC's strategy of maintaining its production at 30 MMBD over an extended period of time will definitely have a knockout affect on some of the US shale basins. The US oil and gas industry is already slashing jobs as a result of the slowdown in drilling/fracturing activities. A lower oil price will discourage shale oil production but it will be stiff call for OPEC to meet the government budgetary requirements.

Table 2: Top ten countries technically recoverable shale gas reserves**

*EIA estimates and for ranking estimates. ARI estimates in parenthesis.

**These shale oil and shale gas resource estimates are highly uncertain and will remain so until they are extensively tested with production wells. This report's methodology for estimating the shale resources outside the United States is based on the geology and resource recovery rates of similar shale formations in the United States (referred to as analogs) that have produced shale oil and shale gas from thousands of producing wells.

Source: US Energy Information Administration (EIA).

In this market share cold war, who will be the winners and losers? The ultimate winner would be producers, however, in the short term consumers will enjoy a period of lower oil prices. This will helping in the revival of global economies. US oil demand is generally stronger during summer driving season and lower gasoline prices will further encourage travelers on the road. China is also taking advantage of lower oil prices in building its stocks.

That is, global oil demand has already shown signs of recovery. What we have learned from history is that neither higher or nor the lower oil prices are sustainable for an extended period of time. A lower oil price environment over an extended period of time will discourage the exploration activities affecting the supply side of the equation while higher oil prices hinder oil demand. With technological advancements and the shale oil revolution one can expect that breakeven cost will keep reducing over time, therefore other conventional oil producers must adjust and learn to live in a new environment of moderate oil prices. We strongly believe that over the longer term market fundamentals will prevail and it is neither a nightmare for OPEC nor for shale oil.

Dr. Salman Ghouri is an advisor for the oil & gas industry

Umama Ghouri is an MBA student at the University of Texas at Arlington, Texas, USA

Image: Oil refinery in Mina-Al-Ahmadi, Kuwait. By: Lokantha CC-By license.

The sustained higher oil prices provided wind falls to major oil producers but at the same time severely affected the global economies, particularly oil importing countries. For oil producing countries more revenues means more resources for the development of their economies and therefore generally ignore its implications for global supply and demand. The sustained higher oil prices not only negatively effected the demand side, it also created a glut in oil market – eventually leading to collapsing oil prices.

Economic development – more reliance on cash cows!

Most of the OPEC members require continuous massive cash flows because they are in the process of economic development. When oil prices are high there are no issues, however when oil prices are suddenly in free fall this poses a real challenge. Challenges for OPEC members in 2015 are even more difficult then they were in the past as they are fighting three conflicting fronts: meeting ever increasing cash flow requirements; defending their market share in a a low oil price environment; and dealing with the competition of the US booming shale oil industry. In the past, OPEC has been pursuing a policy of stabilizing the market by increasing/decreasing production quota but at the same time defending its market share.

For example, strategy in 2015 is different from the one in the 1980s when OPEC increased its production to regain its lost market share due to significant increase in Norway and UK oil production, resulting in collapsing oil prices in 1986. Whilst in 2008, OPEC twice cut its production in an effort to arrest the free fall of oil prices. During recent meetings OPEC has been maintaining a production quota of 30 MMBD as oil prices remained above $100/BBL and even when oil prices plunged below $60/BBL. For example, during the 166th meeting held on Nov 27, 2014 and the 167th on June 5, 2015, OPEC members unanimously agreed that the global oil market is well supplied, inventories are higher than the previous five years average and therefore they would stick with 30 MMBD production quotas.

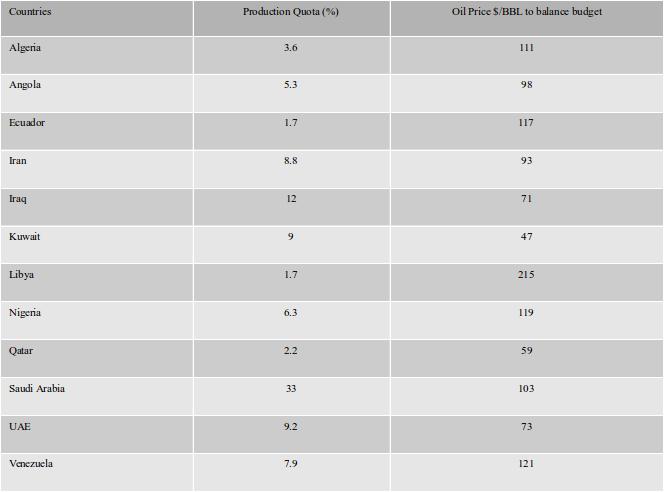

The next meeting will be held on Dec 4, 2015. With this announcement the element of uncertainty is reduced and one can see the determination and commitment of OPEC members to defend their market share even at the cost of lower oil prices. OPEC probably isn't interested in further increasing its production like in the 1980s or cutting its production for a revival of oil prices (2008). The problem is that OPEC is now facing a Catch-22 situation. On the one hand OPEC members need more revenues to meet their ever increasing government budgetary requirements but lower oil prices prevent that from happening. On the other hand if OPEC cuts its production in an effort to revive oil prices it is threatened by losing market share to US shale oil. At oil prices of, for example, $65/BBL (Brent May 2015) OPEC members would be needing substantial higher oil prices to balance their budget (see Table 1). Only Kuwait and Qatar would be in a position to meet their cash flow requirements, the other members would have to produce more or withdraw from sovereign funds in order to balance budget.

Table-1: OPEC production based on quota and oil prices to balance budget*

*The respective shares of the group’s supply are based on April levels. The estimates for the price per barrel each member needs to balance its budget are from the International Monetary Fund unless stated otherwise.

Source: Gulf Times: Saudi oil strategy seen prevailing in Vienna: OPEC reality check

More challenges for OPEC

So far so good. OPEC is successfully maintaining its production quota of 30 MMBD (though there is news they are producing more) that allows it to maintain its market share, and also deter the rising US shale oil production threat. The real challenge however, for OPEC, is how to deal with Russian increasing oil supplies. Russia hit hard by sanctions, requires more revenues to aid its crippling economy – by increasing its oil production. According to Bloomberg in May 2015, it extracted 10.7 MMBD, compared with Saudi Arabia’s 10.2 MMBD. It was the first time Russia took the global lead since 2010.

In addition to Russian oil supplies, another challenge for OPEC is how to deal within its own group. That is, what will happen when economic sanctions on Iran are lifted? A number of countries/companies are already lining up in Iran to seize this investment opportunity. Experts estimate it will take a year or so before Iranian oil production of over one MMBD will hit the market (there are divergent views about quantity and timing). And what would happen if the situation in Libya and Iraq would also simultaneously improve? What would be the implications for global oil supplies and the other OPEC members? Iran and other war torn countries would require huge cash flows for the redevelopment of their economies. How will they finance that? By selling more oil than the allocated quota in a regime of lower oil prices.

More oil supplies from OPEC and Russia are likely to further depress oil prices and this probably temporarily reduces some of the US high cost shale oil production. As a consequence OPEC members face the difficult question how to provide the desired cash flows to their respective governments. In the absence of resilient global oil demand OPEC members will have to dip into their sovereign funds. If OPEC members adhere to production quotas and keep oil prices below the magic number of $60/BBL it will probably discourage US shale oil production at least in some of the basins as well as discourage shale oil development in rich resource countries like China (Table 2). Just like technological advancement in horizontal drilling and hydraulic fracturing turned out to be a nightmare for OPEC, OPEC's strategy of maintaining its production at 30 MMBD over an extended period of time will definitely have a knockout affect on some of the US shale basins. The US oil and gas industry is already slashing jobs as a result of the slowdown in drilling/fracturing activities. A lower oil price will discourage shale oil production but it will be stiff call for OPEC to meet the government budgetary requirements.

Table 2: Top ten countries technically recoverable shale gas reserves**

*EIA estimates and for ranking estimates. ARI estimates in parenthesis.

**These shale oil and shale gas resource estimates are highly uncertain and will remain so until they are extensively tested with production wells. This report's methodology for estimating the shale resources outside the United States is based on the geology and resource recovery rates of similar shale formations in the United States (referred to as analogs) that have produced shale oil and shale gas from thousands of producing wells.

Source: US Energy Information Administration (EIA).

In this market share cold war, who will be the winners and losers? The ultimate winner would be producers, however, in the short term consumers will enjoy a period of lower oil prices. This will helping in the revival of global economies. US oil demand is generally stronger during summer driving season and lower gasoline prices will further encourage travelers on the road. China is also taking advantage of lower oil prices in building its stocks.

That is, global oil demand has already shown signs of recovery. What we have learned from history is that neither higher or nor the lower oil prices are sustainable for an extended period of time. A lower oil price environment over an extended period of time will discourage the exploration activities affecting the supply side of the equation while higher oil prices hinder oil demand. With technological advancements and the shale oil revolution one can expect that breakeven cost will keep reducing over time, therefore other conventional oil producers must adjust and learn to live in a new environment of moderate oil prices. We strongly believe that over the longer term market fundamentals will prevail and it is neither a nightmare for OPEC nor for shale oil.

Dr. Salman Ghouri is an advisor for the oil & gas industry

Umama Ghouri is an MBA student at the University of Texas at Arlington, Texas, USA

Image: Oil refinery in Mina-Al-Ahmadi, Kuwait. By: Lokantha CC-By license.

Read full article

Hide full article

Discussion (0 comments)