The 2014 Ukrainian crisis: Europe's increased security position

on

The 2014 Ukrainian crisis: Europe’s increased security position

For those following the evolution of the energy sector, 2014 has been a year of changes. Tensions have increased, dropped and moved from one segment to another with deals that had been in the air for the last decades being formalised in the midst of these ups and downs. At the core of these turns have been the tense relations between Russia and Ukraine that raised fears of an interruption such as the one in 2009 repeating in 2014 and later in 2015.

Numerous publications have evaluated such an event to assess its implications and to quantify its effects. The study The 2014 Ukrainian crisis: Europe’s increased security position. Natural gas network assessment and scenario simulations prepared by the Institute of Energy Economics at the University of Cologne (EWI) is part of these efforts. It aims at understanding Europe’s security position in regards to natural gas imports transiting Ukraine. For this, it combines a detailed analysis of Europe’s natural gas sector with scenario simulations prepared with the TIGER Model to quantify the consequences of such a disruption. Although it concludes Europe’s security has increased since 2009, the study examines too the challenges ahead for sustaining these gains.

Main findings

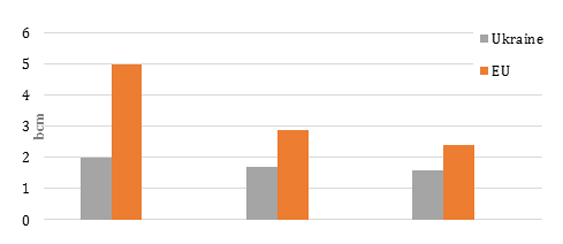

The study concludes that while Ukraine is currently not able to obtain sustainable gas supplies without external financing or drastic reductions of its demand, Europe is in a better positioned compared to 2009. It continues to be dependent on this import corridor on a yearly basis, but on the short run (e.g. less than 3 months), it has achieved notable security of supply gains. A similar disruption to the one in 2009 has been modelled and results show that non-delivered gas volumes to the EU would decrease by 50% (from 5 bcm to 2,4 bcm).

|

| Chart: Total non-delivered supplies to Ukraine and Europe during the 2009 disruption, and during a similar simulated 2-week disruption in 2015 - Source: IEA (2014) and TIGER Model |

Several factors contribute to this outcome:

- First, Europe’s demand has underperformed projections in the last 5 years. This has resulted in infrastructure in place capable of meeting demand levels above current consumption by 100 to 200 bcm, providing spare capacity for the event of an emergency.

- Second, access to alternative supplies has improved. Pipeline import capacity has greatly increased in Central Europe due to the commissioning of the Nord Stream in 2012. At the same time, large storage capacity additions provide a greater security margin for short-term disruptions. Storage volumes in 2014 reached the highest levels ever recorded in Europe with +10 bcm more gas in stock than any previous year. Regarding LNG, current market data indicates that the global market has recently become more flexible to adapt to emergencies. Added up, these sources compensate for the 25 bcm/y decrease recorded in EU indigenous production in the 2009-13 period (84 bcm decrease if we look at the 2001-13 period)

- Third, transport infrastructure capacity has increased in the 2009-14 period resulting in greater cross-border capacity. Up to 40% of border points include now bidirectional capabilities up from 15% in 2009. These additions allow better distributing alternative gas sources from storage, LNG and import pipelines.

- Fourth, since 2009 Europe has implemented more consistent and ambitious security of supply regulation including common security standards, coordination mechanisms and investment funds.

Despite this optimistic outlook, Europe’s security of supply position should be balanced by looking at the not so optimistic underperformance of its natural gas sector.

| the natural gas sector’s decline feeds Europe’s security gains |

How vulnerable is EU to interruptions in Ukrainian transit?

In 2013, Gazprom sales to EU-28 represented up to 29% of total EU consumption and 14% of Europe’s demand was served through Ukraine. Despite Europe being largely supplied by Russia, it is less vulnerable to gas disruption through its main import route (Ukraine) than in 2009.

The risk of supply disruptions resulting from interruptions in Ukrainian transit is regionally narrower. Compared to 2009, exposure is geographically more limited and applies to smaller markets. Out of the five EU largest natural gas markets with demand above 30 bcm/y (Germany, the UK, Italy, Netherlands, France and Spain), only Italy imported more than 15% of its consumption via Ukraine in 2014. Germany used to be the largest market with a large exposure to this route, but this has changed with the commissioning of the Nord Stream pipeline. The UK, Netherlands, France and Spain consume little or no gas transiting this route.

Countries recording greater import levels from gas transiting Ukrainian transit are all small gas markets with annual consumption below 10 bcm/y. Bulgaria, Hungary, Austria, Slovakia and the Czech Republic import a large share of their consumption from this route, although only Bulgaria has insufficient infrastructure capacity to substitute this source. Finally, Serbia, Macedonia and Bosnia Herzegovina, which were greatly affected by the 2009 disruption, remain to be highly reliant on Ukraine to supply their domestic markets.

Scenario simulations show Ukraine, Bulgaria, Turkey and Macedonia would be hit hardest by a disruption

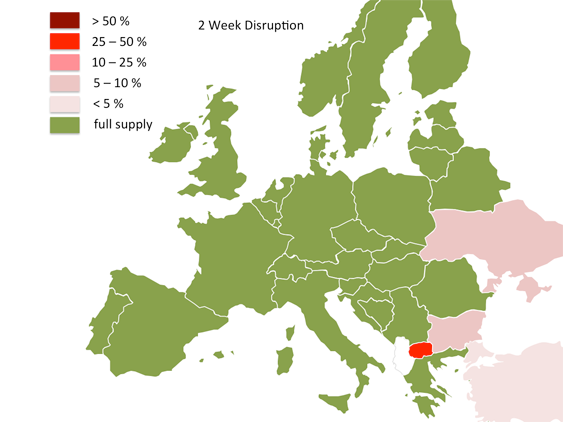

A numerical analysis of different Ukrainian disruption scenarios with the TIGER model enable detailed quantification of the gas system’s resilience during a supply crisis. These scenarios vary both in regards to the duration of the disruption and the winter temperatures. Simulation results allow pointing out seven important findings:

First, non-delivered gas during a modelled disruption similar to that of 2009 comes down from 5 bcm to 2,4 (2,9 bcm if we consider exceptionally low temperatures).

|

|

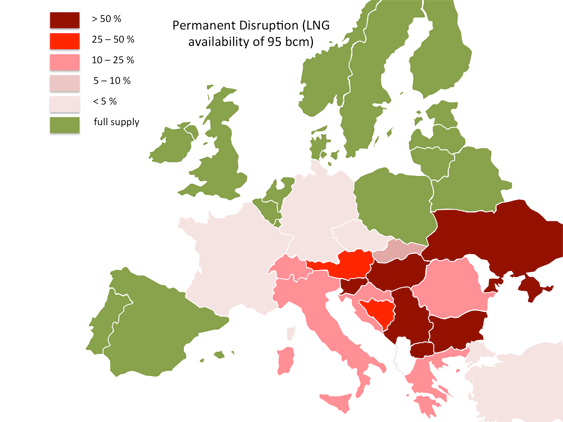

| Maps: Supply shortfalls in the 2-week and 1-year disruption scenarios. - Note: The first map represents maximum daily unserved demand. The second map represents the percentage of annual unserved demand. |

Second, modelling results indicate that shortfalls are limited compared to the 2009 crisis and that the number of exposed countries remains constant despite changes in scenario durations. During the modelled 2-week, 3-month and 6-month disruptions demand is not fully satisfied to variable degrees in Ukraine, Turkey and Macedonia and Bulgaria.

Third, simulations including cold spells result in critical shortages in Bosnia Herzegovina, Bulgaria, Greece, Italy, Macedonia, Turkey and Ukraine

Fourth, LNG imports play a key role compensating non-delivered gas. This is specially the case in South-East Europe, i.e., Italy, Turkey and Greece, although limitations in pipeline capacity reduce the compensation potential of this source. Results show that LNG imports compensate 2.5 bcm per month during a 3-month disruption, and 3.5 bcm per month during a 6-month disruption. Additionally, LNG is crucial in the aftermath of the crisis to re-fill storage facilities.

Fifth, modelling results also show the key role storage plays during all modelled disruptions. Both in the 2-week and the 6-month scenarios, storage withdrawals in Ukraine and Italy (as well as Czech Republic, Slovakia, Hungary and Austria) provide the largest additional gas supplies.

Sixth, a comparative analysis of compensation quantities shows the role different supply sources play. During a 6-month disruption not delivered gas through Ukraine between November and April amounts to 51.4 bcm. This volume is compensated with extensive storage withdrawal of 21.5 bcm, additional LNG imports of 15.6 bcm and additional European indigenous production amounting to 1.8 bcm. Total unserved demand amounts to 12.4 bcm (Ukraine and Turkey included).

Seventh,

| This shows Europe’s inability to diversify away from Ukraine during longer periods of time |

Russia and Ukraine’s resulting position

Russia has depended on Ukraine for a large share of its exports to Europe (Turkey included). Despite the corridor’s lower utilisation in the recent years, it still relies on Ukraine for exporting natural gas volumes beyond 88 bcm.

Ukraine has traditionally depended on Russian supplies and continues to do so. According to modelling results, an interruption of these supplies during the winter season lasting for more than 2 weeks would result in severe shortfalls. Reverse gas flows from European countries help reducing the severity of the interruption but are not sufficient to fully substitute Russian deliveries to Ukraine.

So what? Challenges ahead for Europe and its energy sector

While the study points out the favourable security position Europe holds vis-à-vis Ukraine, it concludes too that factors contributing to this outcome are not all positive. Demand projections for the 2009/14 period have not been realised and have resulted in large infrastructure in place in storage, regasification and transmission. The absorption of this decrease has been different in each of the segments leading to challenges of its own.

- Storage facilities have decreased in number in 2013 and this trend can continue at current market conditions. In the medium-to-long-term this could result in a decrease of storage capacity that has been one of Europe’s key security guarantees in 2014/15.

- LNG terminals have decreased regasification rates from 40% in 2010 to 18% in 2013. Changes in LNG markets might draw a more positive outlook in the medium term.

- Transmission operators face a different situation as the segment is mostly regulated within Europe. However, changes in supply patterns within Europe (especially in Eastern Europe) pose challenges to both regulation and investment.

As infrastructure operators adjust to current demand levels, questions regarding Europe’s capacity to maintain current energy security levels will emerge.

| Can infrastructure operators generate cash flows to build, maintain and operate overcapacity under the current gas market design? |

While the current study focuses on EU-Ukrainian transit dependence, its conclusions surpass Europe’s borders. At the time of writing, Russia, Ukraine, and the EU are preparing tripartite talks to settle the terms of Russia’s gas supplies to Ukraine once the “Winter Gas Package” expires in March 2015. While Russia expressed its intent to continue with 2009-2019 contracts, Ukraine anticipates the reversal of this framework. Kiev’s ambitions to free itself these obligations looks to Europe as an alternative. This is a significant development for Europe that could bring additional changes to its gas industry as Slovakia’s and other interconnections open up opportunities to re-arrange supply logistics in Eastern Europe.

Changes in East and South East Europe are likely to be affected too by Russia’s expansion’s plans and by its recent cancellation of the South Stream pipeline. The substitution for an alternative pipeline to Turkey continues to leave uncertainty for gas supplies to Europe’s most exposed regions to supply interruptions.

| Disclaimer: The responsibility for this analysis lies solely with the authors. Any views expressed are those of the authors and do not necessarily represent those of the EWI. Miguel Martinez is the project leader for this report. He is a Gas & Power analyst with expertise on Europe. In the past he has lead research at ENEL (Rome) on energy pricing dynamics in EU and MENA. Martin Paletar is a Gas & Power expert who works as a Consultant in Markets & Regulations advisory team at DNV GL – Energy. Dr. Harald Hecking has been the Head of Fuel Market Research at EWI since October 2014. He has been working on gas markets projects, e.g., assessing future potentials of natural gas in Germany and the economics of long-term gas contracts. |

Discussion (0 comments)