For engineers and makers, the exploding cost if paper might be seen as a marginal topic. However, it should concern all of us, since paper is still somehow everywhere. Print publishers and their customers are not immune to this development.

For engineers and makers, rising paper costs might be seen as a marginal topic. However, it should concern all of us, since paper is still somehow everywhere. Print publishers and their customers are not immune to this development.

One might hastily try to explain this with something like: “Well, it’s not just chips that are short in supply!” Or: “So, the onset of inflation has also hit the paper market!” But there is more to it than meets the eye. First of all, in central Europe and other industrialized countries, the production of pre-paper products like wastepaper, pulp, etc. — and this is the scarce resource we are talking about here — does not cover the actual demands. Hence, paper and paper precursors have already been imported on a significant scale for a long time. This creates dependencies that — in times of difficulties with logistics, supply chains and production volumes — become problems inevitable leading to increased prices.

Paper Costs: The Current Situation

For almost a year now, there have been signs pointing to the threat of a cost explosion in the paper market. You can easily find online articles — such as, “Pandemic causes paper prices to rise (German)” — detailing how many suppliers have had to increase their prices by up to 20% already in March 2021. And this might just be the beginning.

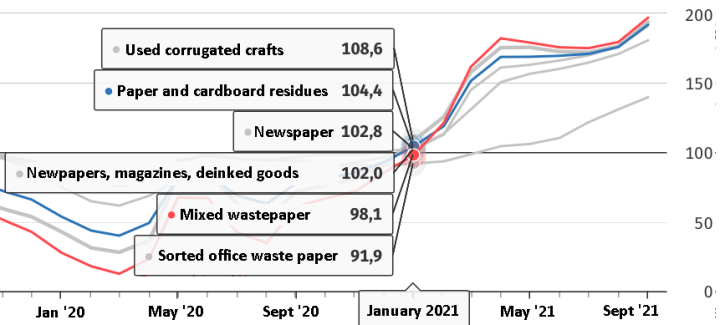

The development of wholesale prices for wastepaper in the first three months of 2021 (2015 = 100%). Source: Federal Statistical Office of Germany (Destatis) 2022.

After prices remained quite stable for several years, the price of wastepaper almost doubled from January to September 2021, and the price for pulp increased by about 50% in the same period, as illustrated in the nearby diagram (according to the German Federal Statistical Office). Since then, a few more months of further hefty price increases have been observed. These prices are transported to, for example, costs of product packaging and increased by just under 20% for general printed paper products (slightly damped only by falling demands of about -23% in this sector during the last 10 years).

Further Inflaters

In Germany, for example, most paper products are based on material from wood-exporting countries like Brazil (share of 22.9%), Sweden (share of 18.3%), and Finland (14.3%). The market is tight — not just because of the global Coronavirus crisis. Already in 2020, more than 75% more paper (compared to the year before) had been exported to Asia. If there is a shortage of material at just a single local point, the effects can quickly become a global issue. According to “Le Monde diplomatique (German)” workers in the Finnish paper industry have been on strike since the beginning of the year. The strike was initially supposed to last until February 19 of this year and was temporarily extended by three weeks until March 12 at the beginning of February. Even if this only shuts down a small part of the global production capabilities, it is easy to imagine what effect this will have on prices. For the first quarter of the year, and without the consequences of this strike, the prices for European printing rose by 50% to 70% compared to the previous year.

Aftermath

You do not have to be a fortune teller to predict that paper prices will continue to rise later this year due to the Finnish strike. This also affects large areas of industries that typically have little contact to paper processing but cannot continue operating without packaging materials, printed instructions, cellulose filters, and so on. Hence, paper prices will continue to drive the current inflationary developments.

Obviously, the publishers of printed media are particularly affected by the prince increases. Physical products like printed books, newspapers, and magazines will continue to become more expensive in contrast to virtual online sales channels. Most likely, the publisher will not be able to absorb these immense const increases and will also have to adjust their prices for selling printed products.

Elektor Magazine has been one of the leading sources of information on electronics for engineers, designers, start-ups and companies for 65 years. Our magazine is powered by an active community of electronics engineers – from students to professionals – who are passionate about designing and sharing innovative ideas.

For them, we publish hundreds of items a year, in formats such as articles, videos, webinars, and other learning formats. Our mission is to share knowledge in every possible way and inspire readers with the latest developments within the electrical engineering sector.

Thank you for your vote!

Leave further comments in the fields below.

Thank you for your vote!

If you wish to leave a comment with your rating, please first use the login below. If not, just close this window.

Discussion (0 comments)