Global Chip Market: 2024 Surge Followed by 2025 Slowdown

November 25, 2024

on

on

The global chip market is poised for remarkable growth in 2024, with Semiconductor Intelligence (SC-IQ) forecasting a 19% annual increase, reports Peter Clarke at eeNews Europe. However, SC-IQ predicts a significant slowdown to just 6% growth in 2025, citing decelerating AI demand and broader market weaknesses.

In 3Q24, the chip market soared to $166 billion, marking a 23.2% increase compared to 3Q23. Yet, for 4Q24, SC-IQ calculates a modest 3% growth, reflecting stark contrasts across sectors. Companies focused on AI and data centers, like Nvidia, are thriving, while those serving the automotive and industrial markets face challenges.

"The balance between the market-driving impact of Nvidia and AI versus geopolitical tension and sluggishness in industrial and automotive markets is tipping away from AI’s ability to drag the market up," SC-IQ states. This shift suggests weaker growth prospects in 2025.

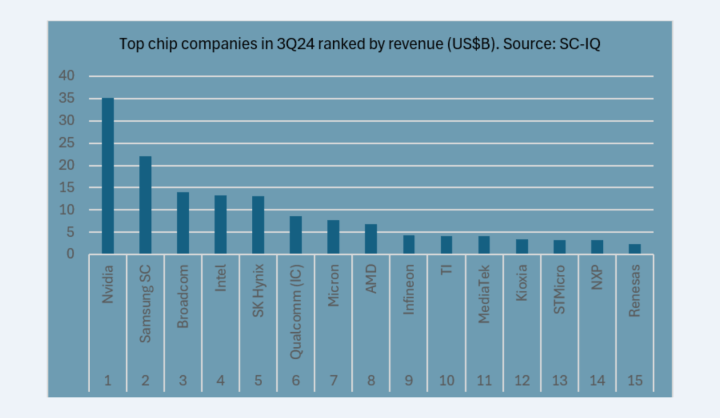

Meanwhile, Intel continues its downward trajectory. Once the world’s leading chip vendor, Intel slipped to fourth place in 3Q24. SC-IQ projects SK Hynix will surpass Intel in 4Q24, cementing the Korean firm's growing influence.

SC-IQ’s 2025 outlook includes the following, Clarke notes:

• Continued AI growth with moderating demand

• Stabilizing memory prices despite healthy AI-driven demand

• Mediocre smartphone and PC growth

• Weakness in the automotive market

• Potentially higher U.S. tariffs affecting consumer demand

As geopolitical and market dynamics shift, 2025 may test the resilience of the global chip industry.

Editor's note: Our colleague Peter Clarke first reported on this in EENews Europe, a publication in the Elektor network.

In 3Q24, the chip market soared to $166 billion, marking a 23.2% increase compared to 3Q23. Yet, for 4Q24, SC-IQ calculates a modest 3% growth, reflecting stark contrasts across sectors. Companies focused on AI and data centers, like Nvidia, are thriving, while those serving the automotive and industrial markets face challenges.

"The balance between the market-driving impact of Nvidia and AI versus geopolitical tension and sluggishness in industrial and automotive markets is tipping away from AI’s ability to drag the market up," SC-IQ states. This shift suggests weaker growth prospects in 2025.

Subscribe

Tag alert: Subscribe to the tag artificial Intelligence and you will receive an e-mail as soon as a new item about it is published on our website! Nvidia’s Dominance and Intel’s Decline

Nvidia emerged as the largest chip company in 3Q24, posting $35.1 billion in revenue, driven by its strength in AI GPUs, Clarke reports. While this figure includes memory sourced from SK Hynix, Micron Technology, and Samsung, SC-IQ notes Nvidia remains the top player even after adjusting for double-counting.Meanwhile, Intel continues its downward trajectory. Once the world’s leading chip vendor, Intel slipped to fourth place in 3Q24. SC-IQ projects SK Hynix will surpass Intel in 4Q24, cementing the Korean firm's growing influence.

Subscribe

Tag alert: Subscribe to the tag Nvidia and you will receive an e-mail as soon as a new item about it is published on our website! 2025: AI Still a Driver, But Growth Moderates

While AI will remain a key growth driver, SC-IQ anticipates slowing momentum. Servers, smartphones, and PCs will contribute to chip demand, with PCs showing a modest 4.3% growth in 2025 compared to just 0.3% in 2024, according to IDC.SC-IQ’s 2025 outlook includes the following, Clarke notes:

• Continued AI growth with moderating demand

• Stabilizing memory prices despite healthy AI-driven demand

• Mediocre smartphone and PC growth

• Weakness in the automotive market

• Potentially higher U.S. tariffs affecting consumer demand

As geopolitical and market dynamics shift, 2025 may test the resilience of the global chip industry.

Subscribe

Tag alert: Subscribe to the tag Embedded & AI and you will receive an e-mail as soon as a new item about it is published on our website! Editor's note: Our colleague Peter Clarke first reported on this in EENews Europe, a publication in the Elektor network.

Read full article

Hide full article

Discussion (0 comments)